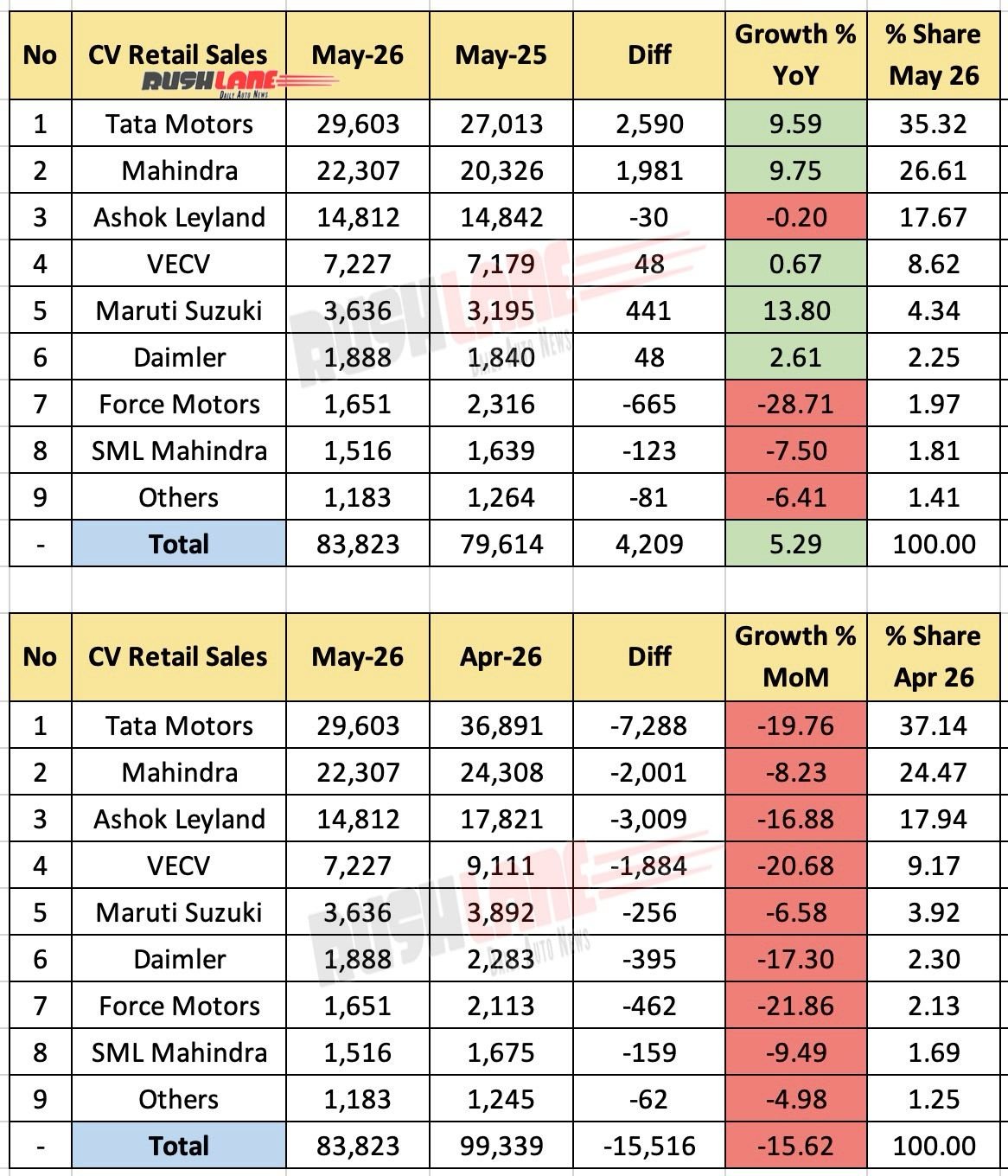

Commercial vehicle retail sales in India recorded moderate growth in May 2026, mainly supported by Tata Motors and Mahindra. Total CV retail sales stood at 83,823 units, up 5.29% compared to 79,614 units sold in May 2025. However, on a month-on-month basis, the industry witnessed a sharp decline of 15.62% from 99,339 units retailed in April 2026.

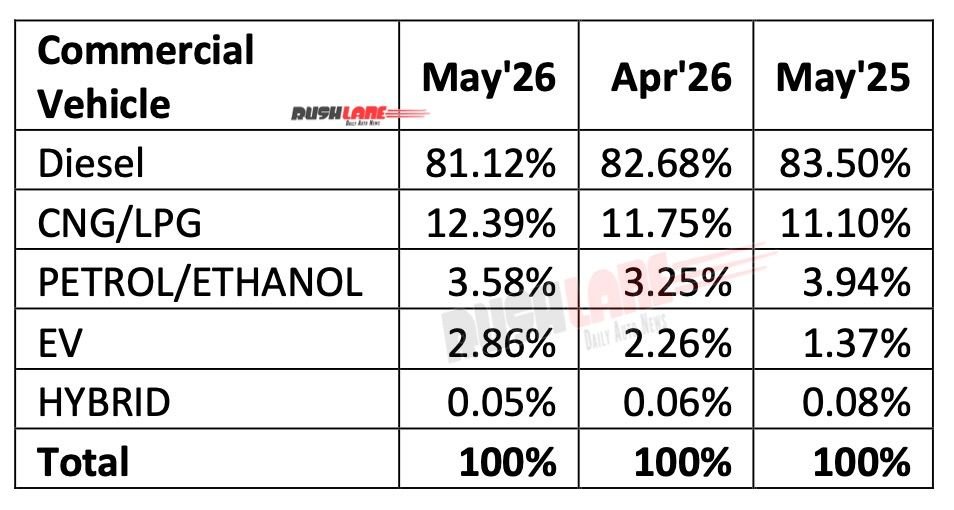

Fuel wise CV sales May 2026

Diesel continued to dominate India’s commercial vehicle market in May 2026, accounting for 81.12% of total retail sales. However, its share has gradually declined from 83.50% in May 2025 to 82.68% in April 2026, indicating a slow shift towards alternative fuel options. The share of CVs running on CNG and LPG increased to 12.39% from 11.10% a year ago, while EV adoption also accelerated.

The share of electric commercial vehicles in total retail sales in May 2026 was 2.86%, more than double their share of 1.37% in May 2025. Petrol and ethanol-powered vehicles contributed 3.58%, while hybrids remained negligible at only 0.05%. The data shows that although diesel remains the backbone of the commercial vehicle industry, alternative powertrains—particularly CNG and electric—are rapidly gaining popularity.

CV Retail Sales May 2026

Tata Motors continued its dominance in the commercial vehicle retail sector with sales of 29,603 units in May 2026. The company registered a healthy growth of 9.59% year-on-year, adding 2,590 units as compared to May last year. Tata maintained its leading position with 35.32% market share, more than eight percentage points ahead of Mahindra.

Mahindra remained the second largest CV company with retail sales of 22,307 units, registering a growth of 9.75% YoY. The company added 1,981 units in May 2025 and increased its market share to 26.61%. Mahindra’s growth rate is slightly higher than Tata Motors on a percentage basis, indicating continued momentum in its commercial vehicle business. However, like most OEMs, Mahindra also experienced a MoM decline of 8.23%.

Ashok Leyland retained the third position with sales of 14,812 units in May 2026. Sales remained largely stable compared to last year, with a slight decline of 0.20% year-on-year. The company’s market share during the month stood at 17.67%. Month-on-month, Ashok Leyland volumes declined by 16.88%, reflecting the broader slowdown seen in the CV market.

VECV, Maruti Suzuki Post Growth

VE Commercial Vehicles (VECV) recorded retail sales of 7,227 units registering a marginal growth of 0.67% YoY. The company had 8.62% market share. Maruti Suzuki continued to expand its presence in the commercial vehicle segment with sales of 3,636 units, a growth of 13.80% year-on-year.

Among the key players, Maruti recorded strong growth, highlighting steady demand for its Super Carry range. Daimler India Commercial Vehicles also recorded a positive growth of 2.61% YoY with retail sales of 1,888 units. The biggest decline was recorded in Force Motors. Retail sales fell 28.71% year-on-year to 1,651 units, down from 2,316 units sold a year ago. SML Mahindra also recorded negative growth, with sales declining 7.50% year-on-year to 1,516 units.

Industry sees decline in broad-based MOM

While the year-on-year performance remained positive, May 2026 saw a significant deceleration compared to April 2026. Total industry retail volumes declined by 15,516 units, translating into a 15.62% MoM decline. Every major OEM reported lower volumes than April. Tata Motors, VECV, Force Motors and Daimler all recorded double-digit percentage declines, indicating soft market conditions during the month.