CV Retail Sales February 2026 – Tata leads the market with 28.9% YoY growth

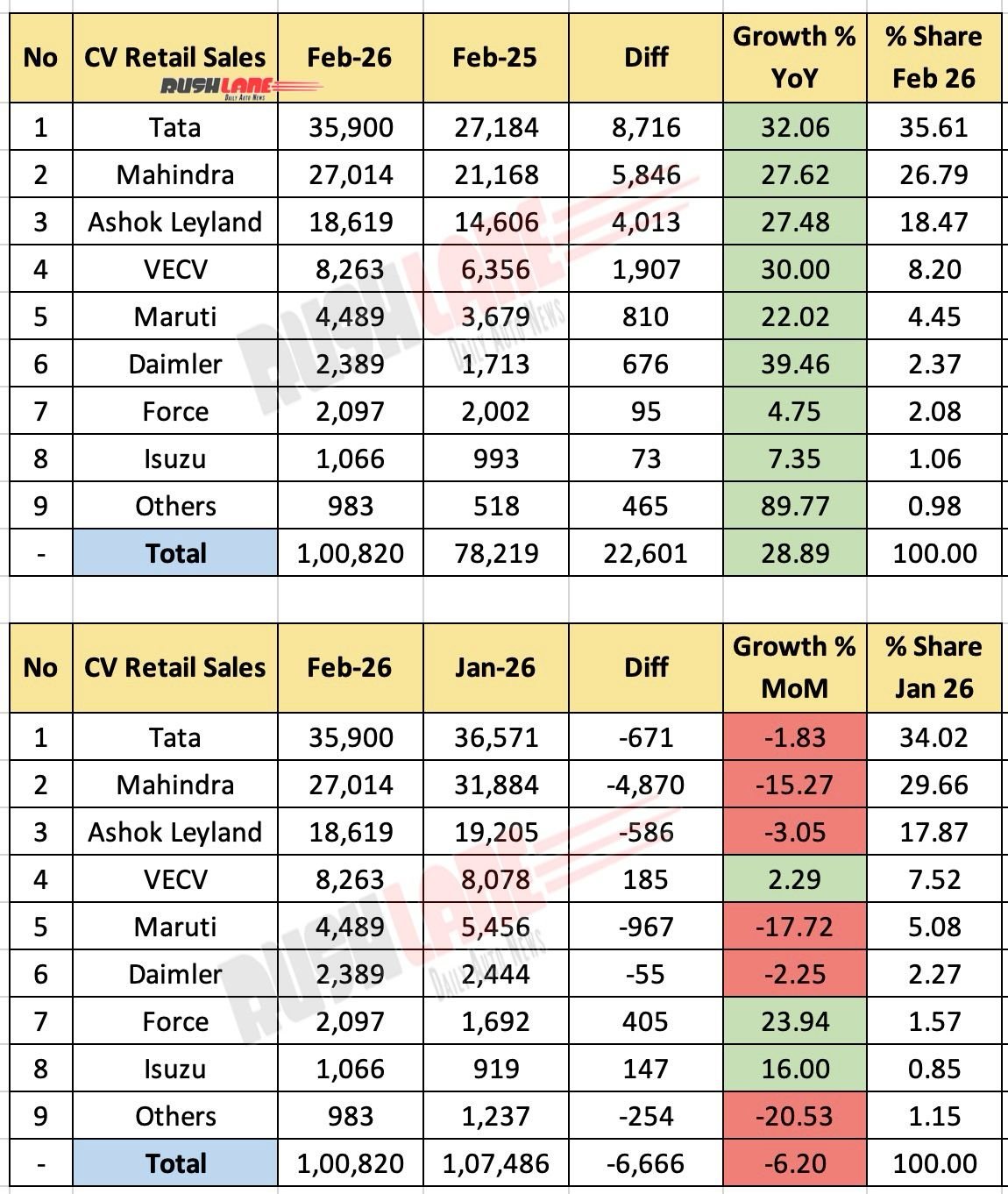

India’s commercial vehicle (CV) segment recorded strong year-on-year growth in February 2026, supported by improving infrastructure activity, stable rural demand and continued movement in the logistics and construction sectors. According to data released by the Federation of Automobile Dealers Associations (FADA), total CV retail sales stood at 1,00,820 units in February 2026, registering a 28.89% year-on-year growth as compared to 78,219 units sold in February 2025. However, on a month-on-month basis, sales declined by 6.20% compared to 1,07,486 units sold in January 2026, reflecting normal. Seasonal fluctuations followed by strong demand at the beginning of the year.

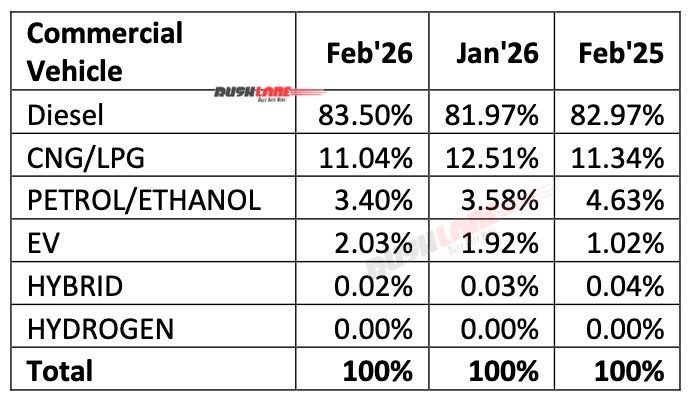

Diesel continues to dominate CV powertrains

Diesel remains the dominant fuel type in the commercial vehicle segment. In February 2026, the share of diesel-powered CVs in total sales stood at 83.50%, slightly higher than the 82.97% recorded in February 2025. The market share of CNG and LPG vehicles stood at 11.04%, while the share of petrol/ ethanol driven CVs was 3.40%. Electric commercial vehicles continued to gradually gain traction with the share increasing from 1.02% to 2.03% in February 2025. The share of hybrid powertrains was a modest 0.02%, while hydrogen-powered vehicles were not recorded in retail sales.

Tata Motors remains the leader in the CV market

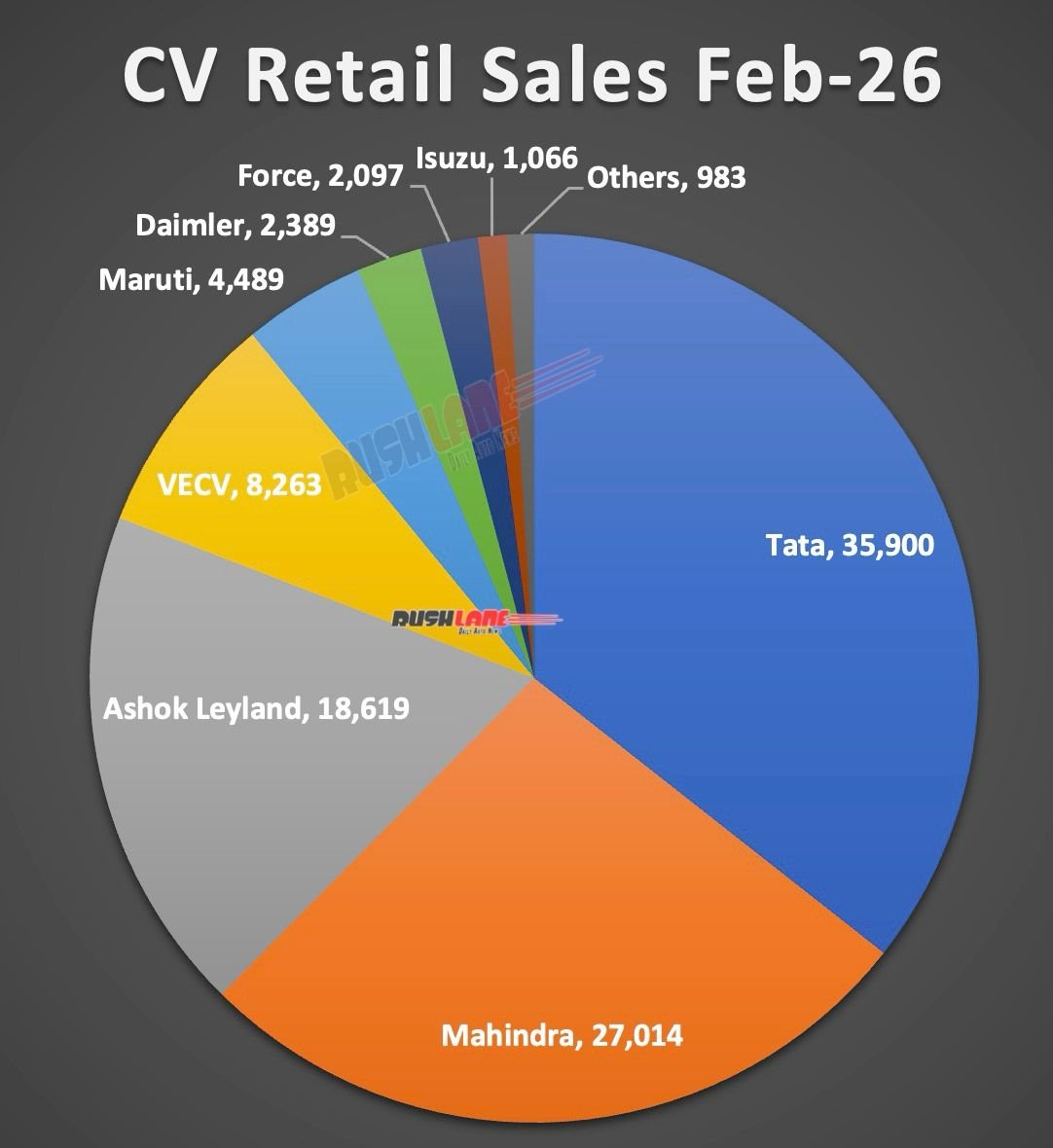

Tata Motors retained its leadership in the commercial vehicle segment with sales of 35,900 units in February 2026, showing a 32.06% YoY growth as compared to 27,184 units sold in February 2025. The company achieved 35.61% market share maintaining a clear lead over its competitors.

Mahindra ranked second with 27,014 units, registering a 27.62% year-on-year growth as compared to 21,168 units sold in the same month last year. Mahindra’s market share stood at 26.79%, primarily driven by its strong presence in the LCV segment and last-mile mobility solutions. Ashok Leyland took the third position with sales of 18,619 units as compared to 14,606 units in February 2025, registering 27.48% year-on-year growth. The company achieved 18.47% market share in the overall CV segment.

VE Commercial Vehicles (VECV) recorded 8,263 units in February 2026, showing 30% YoY growth as compared to 6,356 units last year. The company’s market share during the month stood at 8.20%. Maruti Suzuki recorded 4,489 units with its Super Carry LCV, a growth of 22.02% YoY as compared to 3,679 units sold in February 2025.

Daimler India Commercial Vehicles also recorded strong growth with 2,389 units, up 39.46% compared to 1,713 units last year. Force Motors reported 2,097 units, marking a growth of 4.75% YoY, while Isuzu reported 1,066 units, a growth of 7.35% YoY. Other manufacturers together contributed 983 units, registering an increase of 89.77% from 518 units sold in February 2025.

Mother’s sales saw a slight decline

While the overall CV segment saw strong year-on-year growth, the month-on-month performance was mixed. Tata Motors sales declined by 1.83% MoM compared to January 2026, while Mahindra sales saw a sharp decline of 15.27%. Ashok Leyland also registered a decline of 3.05% MoM, while VE Commercial Vehicles registered a growth of 2.29% MoM. Force Motors and Isuzu also recorded positive MoM growth during the month. Overall CV retail sales declined by 6.20% MoM, indicating moderation after a strong January performance.

With infrastructure spending, e-commerce logistics and rural transportation demand continuing to support the sector, the commercial vehicle segment is expected to maintain a steady pace in the coming months, although global geopolitical developments and fuel price volatility may impact demand trends.